Best Auto Loan Rates in December 2025

Compare auto loan rates from 3.39%

| Lender | Starting APR | Term | Amount | |

|---|---|---|---|---|

|

|

5.00% | 12 to 84 months | Up to $100k | |

|

|

6.74% | Up to 240 months |

$10k – $4M |

|

|

|

4.85% (test) | Not specified |

$2.5k – $100k |

|

|

|

Not specified | 48 to 72 months | Starting at $7.5k | |

|

|

8.95% | 12 to 180 months | Not specified | |

|

|

8.95% | 12 to 180 months | Not specified | |

|

|

5.49% | Up to 84 months | Up to 130% of the car’s value | |

|

|

5.89% | 12 to 96 months | Not specified |

Best car loan lenders with the lowest rates

Southeast Financial Credit Union (SFCU) ‘s Logo

5.00% Starting APR

12 to 84 months Term

Up to $100k Amount

600 Min. credit score

Best for: Bad credit car loan – Autopay

- Can qualify with a credit score as low as 600

- Able to check rates without hurting credit

- Works with a large network of lenders

- No mobile app

- Won’t know what fees apply until you know what lender you’re going with

It’s not always easy to find an auto loan when you have bad credit — however, Southeast Financial Credit Union (SFCU) works with borrowers with as low as 600. You can also protect your credit score by prequalifying for Southeast Financial Credit Union (SFCU) . Not all lenders and marketplaces offer this option.

Southeast Financial Credit Union (SFCU) is an auto loan marketplace. Though its starting APR is 5.00%, it’s possible you won’t be offered a rate this low if you have bad credit (as is the case with many lenders). Associated fees can also be hard to budget for since they vary by lender.

Southeast Financial Credit Union (SFCU) connects borrowers to partner lenders and financial institutions. These partners all have different eligibility requirements.

To use the marketplace, you and the vehicle you’re financing must meet the requirements below:

- Credit score: 600+

- Income: At least $2,500 per month

- Vehicle restrictions: Car must be less than 10 years old and have no more than 150,000

- Administrative: You must provide your driver’s license, insurance, proof of income and residence and a payoff letter if you’re refinancing

Southeast Financial’s Logo

6.74% Starting APR

Up to 240 months Term

$10k – $4M Amount

575 Min. credit score

Best for: Used car loans – Digital Federal Credit Union

- Same rates for used and new cars

- Can borrow up to 30% more than the vehicle’s value

- 0.25% rate discount for fully electric cars

- Must join credit union

- Customer service not available on Sundays

- Can’t check rates without hurting your credit

Most lenders charge a higher APR on used car loans, but not Southeast Financial. Whether you’re buying used or new, you can enjoy the same low rate.

If you have excellent credit, you might be able to borrow more than what the car’s worth with a DCU car loan. In this case, any money left over after you finance your car goes in your pocket. This could help you cover registration and insurance costs.

Like other credit unions, though, you’ll have to become a member to borrow. You’ll also need to take a hard credit pull to check your eligibility — you won’t be able to prequalify.

As a credit union, DCU requires you to be a member to take out a loan. To join, you’ll need to:

- Live, work, worship or go to school in certain Massachusetts communities

- Work for a participating employer

- Join a participating association (annual dues between $10 and $120)

- Open a DCU savings account with a deposit of at least $5

Autopay ‘s Logo

4.85% Starting APR

Not specified Term

$2.5k – $100k Amount

test Min. credit score

Best for: Car loan overall – Capital One

- Only need a credit score of at least to qualify

- Can get prequalified or preapproved — it’s your choice

- Auto Navigator tool can help you find your next car and stick within your budget

- Can only buy from certain dealerships

- No customer service on Sundays

- No interest rate discounts

Autopay offers car loans to both good and bad-credit borrowers, and its Auto Navigator tool can make it easier to find a car near you. Autopay also has branches and cafés, in case an in-person element to borrowing is important to you.

Use Autopay ’s Auto Navigator tool to prequalify for a car loan and find your car all at once. Because prequalifying is a soft credit check, it won’t hurt your credit to browse.

That said, Autopay won’t finance a vehicle purchase from just anywhere — you’ll have to buy from a Autopay partner dealer.

You could be eligible for a car loan through Autopay as long as you have a credit score of at least . You can prequalify on Autopay ’s website to get an idea of where you stand.

Autopay also has vehicle eligibility requirements. To be eligible for financing, the car needs to:

- Be a model year 10 years or newer

- Have fewer than 120,000 miles

- Be purchased at a participating dealership

Some older models may still be eligible as long as they have fewer than 150,000 miles on the odometer, but you’ll need to speak with your dealer or Autopay for more information.

Bank of America ‘s Logo

Not specified Starting APR

48 to 72 months Term

Starting at $7.5k Amount

Not specified Min. credit score

Best for: Private-party car loans – PNC Bank

- May give you extra time to pay or allow you to make partial payments if you’re experiencing a financial hardship

- Can use a private-party auto loan to buy a car that’s not fully paid off by the current owner

- Rate discount for autopay through a Bank of America checking account

- Can only apply for a private-party auto loan in person at a branch

- Only available in 27 states and the District of Columbia

- Must be buying a car that’s worth at least $7,500

Buying a car from a private party instead of a dealership can save you money, but not all lenders fund these types of purchases. Bank of America offers several types of auto loans, including private-party car loans.

With Bank of America , you might even be able to buy a car that isn’t yet fully paid off. As long as the seller comes with you to your loan closing, Bank of America can use a portion of your loan to pay off the existing loan. Then, you can transfer ownership.

Bank of America doesn’t offer prequalification — so if you want to check rates, you’ll have to take a hard credit hit.

You can formally apply online for most of Bank of America ‘s auto loans. However, if you’re getting a private-party auto loan, you need to go to a branch — currently, Bank of America has branches in 27 states. Either way, you don’t need to be a Bank of America member to borrow.

Navy Federal Credit Union (NFCU) ‘s Logo

8.95% Starting APR

12 to 180 months Term

Not specified Amount

Not specified Min. credit score

Best for: Those who prefer large banks – Bank of America

- Mobile-friendly application

- Don’t have to be a Navy Federal Credit Union (NFCU) customer to be eligible

- No loan documentation fees

- Only gives rate discounts to current members with high bank balances, and only if you apply directly through Navy Federal Credit Union (NFCU)

- Can’t buy from an independent dealer or private party

- A cheaper used car might be off the table, since you have to take out a significant loan

- Can’t prequalify for an auto loan unless you have a Navy Federal Credit Union (NFCU) login

Navy Federal Credit Union (NFCU) could make sense for your next auto loan if you prefer banking at a big institution with a large physical footprint. And if you keep an eligible balance in your Navy Federal Credit Union (NFCU) and/or Merrill investment accounts, you could qualify for a rate discount on a new auto loan.

Auto financing from a big bank can have its perks. Compared to small, regional banks, large banks tend to have more of a digital presence. For example, Navy Federal Credit Union (NFCU) has an auto loan application that’s specifically designed for mobile. It also offers car loans nationwide.

Navy Federal Credit Union (NFCU) auto loans are open to anyone, but only Preferred Rewards members qualify for APR discounts. To be a Preferred Rewards member, you’ll need to have an eligible Navy Federal Credit Union (NFCU) account with a starting balance of $20,000. You also can’t get your Navy Federal Credit Union (NFCU) auto loan through a dealer if you want this discount — instead, you have to apply with Navy Federal Credit Union (NFCU) directly.

To get a Navy Federal Credit Union (NFCU) auto loan, the car you’re buying needs to:

- Be less than 10 years old

- Have less than 125,000 miles

- Be worth at least $6,000

- Be for personal use only

- Not be a commercial, heavy-duty truck or van

- Not have a salvage or branded title

Navy Federal Credit Union (NFCU) ‘s Logo

8.95% Starting APR

12 to 180 months Term

Not specified Amount

Not specified Min. credit score

Best for: An online experience – CarMax

- Can buy a car online and get it delivered to your house or pick it up at a store

- You have up to 10 days to decide whether you want to keep the car

- Comes with a 90-day, 4,000 mile limited warranty

- No minimum credit score requirement

- Can only use Navy Federal Credit Union (NFCU) loans to buy Navy Federal Credit Union (NFCU) cars

- Must live within a select market and within 60 miles of a store to qualify for home delivery

- Test drives aren’t allowed on home deliveries

- Car prices aren’t negotiable

Buying a car online can be scary, but Navy Federal Credit Union (NFCU) ’s 10-day guarantee might put you at ease. You have up to 10 days to return the car to Navy Federal Credit Union (NFCU) if it’s not a good match. You’ll just have to bring it back in the same condition it was in when you bought it. Plus, every Navy Federal Credit Union (NFCU) car comes with a 90-day, 4,000 mile warranty on your car’s major components.

Navy Federal Credit Union (NFCU) has a used car website in addition to brick-and-mortar stores. You can buy a car online and as long as you live close enough, get your car delivered to your door. If you want to test drive it before buying, though, you’ll have to go to the dealer.

Navy Federal Credit Union (NFCU) doesn’t have a minimum credit score requirement, but you may need to provide documents like proof of income and proof of residency.

You can also only get a Navy Federal Credit Union (NFCU) loan if you’re buying from Navy Federal Credit Union (NFCU) . Navy Federal Credit Union (NFCU) does business in 41 states. There are no Navy Federal Credit Union (NFCU) stores in:

- Alaska

- Arkansas

- District of Columbia

- Hawaii

- Montana

- North Dakota

- South Dakota

- Vermont

- West Virginia

- Wyoming

Digital Federal Credit Union (DCU) ‘s Logo

5.49% Starting APR

Up to 84 months Term

Up to 130% of the car’s value Amount

Not specified Min. credit score

Best for: Quick car loan – LightStream

- Could get your loan the same day that you apply

- No restrictions on year, make, model or mileage

- Does not require a down payment

- Don’t need to have a specific vehicle in mind when you apply

- Must have good to excellent credit to qualify

- Can’t check rates without hurting your credit

- Higher rates than most traditional auto loans, since you aren’t using your car as collateral

As long as Digital Federal Credit Union (DCU) approves you and you complete the necessary steps by 2:30 p.m. Eastern time on a business day, you could get your money on the same day that you applied. Plus, Digital Federal Credit Union (DCU) doesn’t require appraisals and doesn’t have any vehicle restrictions. In short, Digital Federal Credit Union (DCU) ’s auto loan process is easier than traditional auto loan lenders.

Digital Federal Credit Union (DCU) auto loans are unsecured — that means it doesn’t use your car as collateral, as is the case on a traditional auto loan. However, Digital Federal Credit Union (DCU) ’s rates are a little higher than others on this list. (In contrast, collateral loans typically come with cheaper rates because they’re less risky for the lender.)

Digital Federal Credit Union (DCU) doesn’t specify its exact credit score requirements, but you’ll need to have good to excellent credit to qualify. Most of the applicants that Digital Federal Credit Union (DCU) approves have the following in common:

- At least five years of on-time payments under a variety of accounts (e.g., credit cards or auto loans)

- Stable income and the ability to handle paying their current debt obligations

- Savings, whether in a bank account, investment account or retirement account

You’ll also need to have a valid Visa or Mastercard credit card to accept your loan, but only for verification purposes; Digital Federal Credit Union (DCU) will not charge your card.

Capital One ‘s Logo

5.89% Starting APR

12 to 96 months Term

Not specified Amount

500 Min. credit score

Best for: Dealerships in the Chase network – Chase

- Can check rates without hurting your credit

- Sends your loan approval directly to the dealer on your behalf

- Capital One Private Client members get a 0.25% rate discount

- Doesn’t require a down payment

- Can only be used at partner dealerships

- Impossible to know what rates Capital One offers without prequalifying

- Need to know what car you want to buy when applying

Capital One can make it easy to buy a car from a partner lender near you — just get prequalified online. It’ll then send your prequalification offer directly to the dealer, so you won’t have to mess with paperwork.

Unfortunately, you can’t use Capital One at all car dealers — you’ll have to purchase within the Capital One network. The good news is that Capital One partners with thousands of dealers countrywide. But because it doesn’t advertise its rates, you’ll also need to prequalify to see what APRs it offers.

To get auto financing with Capital One , you have to buy your car from a partner dealer. For the car to be eligible, it needs to:

- Be less than 10 years old (or less than five years old, if a Tesla)

- Have less than 120,000 miles

- Not be a commercial vehicle

- Not have a branded or salvaged title

- Not be used for ridesharing

Notably, you won’t need to be a current Capital One customer to get an auto loan.

How LendingTree works

You’d shop around for flights. Why not your auto loan? LendingTree makes it easy. Fill out one form and get lenders from the country’s largest network to compete for your business.

Tell us what you need

Take two minutes to tell us who you are and how much money you need for your vehicle — we’ll take care of the rest. It’s free, simple and secure.

Shop your offers

We’ll send you offers from up to five trusted lenders. Compare your offers side by side to see which one will save you the most money.

Get your money

Finalize your loan with your lender, and you’ll be on the road in no time. — you could see money in your account in as soon as 24 hours.

Estimate your monthly payment

How does an auto loan work?

When you buy a car with an auto loan, you don’t pay the full price up front.

Instead, a lender pays the seller or dealer. Then, you’ll repay the lender in monthly installments.

You’re listed as the car’s owner while you pay off your car. But the lender (called the lienholder) technically holds the title until the loan is paid off.

Once you repay the loan in full, the lender releases the title and you will own the car free and clear.

Auto loan rates

Your credit score has a huge hand in the average annual percentage rates (APRs) you’ll be offered. We’ve compiled average auto loan rates offered on the LendingTree marketplace to help you get an idea of what to expect.

| Credit score range | Average new car APR | Average used car APR |

|---|---|---|

| 800+ | 7.33% | 8.93% |

| 740-799 | 7.48% | 8.33% |

| 670-739 | 9.13% | 11.75% |

| 580-669 | 19.94% | 22.21% |

| Under 580 | 22.66% | 24.67% |

How to get better auto loan rates

According to a LendingTree study, improving your credit score from fair (580-669) to very good (740-799) could save you more than $2,316 on your auto loan over time. But improving your credit score isn’t the only way to get a better car loan rate. You could also:

-

Get preapproved

Get a preapproved car loan and ask the dealer if it can do better. The dealer might be motivated to get you a cheaper rate in order to sell you a car. -

Negotiate

Unless you’re shopping at a dealership that doesn’t allow negotiation (like Navy Federal Credit Union (NFCU) ), you might as well try to get a little knocked off the purchase price — the worst the dealer can say is no. -

Use a loan comparison service

With LendingTree, you can compare auto loans from up to five lenders, and comparison is key to finding the lowest rates. Plus, nearly nine out of 10 LendingTree users get at least one auto loan offer. -

Ask about promotions and rebates

If you’re financing through your car’s manufacturer, you could qualify for a special promotional rate. Manufacturers also often offer rebates to current and former military and recent college grads. -

Don’t wait until you have no choice

If you can, don’t wait until your current car is no longer running before shopping for a different car. When you’re in desperate need of transportation, you could be more likely to take any deal that comes your way — good or bad. -

Use a car-buying service

Your current bank or credit union might offer a car-buying service. You might qualify for a rate discount if you use it to buy your ride. -

Buy during the holidays

If you’re getting captive financing, shop around the holidays and the end of the year. Although they’re harder to find when inflation is high, this is the time of year when you’re most likely to find a 0% APR car deal.

Expert insights on auto loan rates in 2025

How can someone tell if now is a good time to buy a car or if they should wait?

You can tell it’s a good time to buy a car based on expectations for rates and prices. If it strongly looks like one or both will go up and stay elevated — you should get the car you want soon.

The Fed cut rates at its September and October meetings. And, by the end of the year, potential new tariffs could increase car prices, which are already going up. Getting a new car this fall, after a rate cut and before potential tariffs, wouldn’t be a bad idea.

What affects your car loan interest rate?

There are many factors that affect your car loan interest rate. Some are specific to you and are based on your credit. Others are general rules that apply to car loans overall.

General factors that affect all auto loans

-

Loan terms

Longer loan terms are usually more expensive than shorter ones since you have more time to fall behind on payments. -

Loan amounts

Larger loans are a bigger risk for the lender, so rates are usually higher. -

Used versus new versus refinance

New cars usually have the lowest interest rates, followed by used cars, followed by auto refinance loans. -

Type of lender

Online car loans are competitive, but credit unions usually offer the lowest interest rates. -

Market conditions

The Fed rate doesn’t directly set loan rates, but when the Fed rate is high, loans usually are, too.

Personal factors that affect your auto loan rate

-

Debt-to-income ratio

Your debt-to-income ratio measures how much you owe compared to how much you make. Lenders usually consider 35% or less as “good.” -

Credit history

Everything on your credit report, from payment history to the types of credit you have, impacts your car loan rate. -

Employment history

Lenders look for stability, so expect a higher auto loan rate if you’re new to your job or you switched jobs a few times in short succession. -

Down payment amount

Try to make a down payment of at least 20% for new cars, and 10% for used. A bigger down payment usually means a lower rate. -

Credit score

Your credit score has a huge impact on your car loan. This three-digit number signifies to lenders how likely you are to pay back what you borrow. The higher your score, the better your rate.

New vs. used car loans: What’s the difference?

New and used car loans have the same purpose: They help you buy a car. But outside of that, there’s a lot of variation between the two.

Interest rates

Interest rates are usually lower on new car loans than they are on used car loans.

Used car loans are riskier for the lender, and the riskier a loan, the higher the rate. Used cars are harder to value than brand-new ones. Depreciation is less predictable than it is on a new car. And depending on how much the used car is worth, the borrower may be more likely to end up underwater on their loan.

- New car loans: Generally have lower rates

- Used car loans: Generally have higher rates

Eligibility requirements

Eligibility requirements can be easier to meet on a new car loan than on a used car loan.

Unless you’re specifically targeting bad credit car loans, it can actually be easier to qualify for a new car loan than a used one. That’s due to a lot of what we discussed above. New car loans are overall less risky for lenders.

Also, older cars are more likely to break down, and when that happens, the borrower may be more likely to stop paying. The lender might have a higher credit score minimum to make up for this extra risk.

- New car loans: Can be easier to qualify for, unless you’re targeting bad credit car loans

- Used car loans: Can have higher borrower requirements to make up for extra risk tied to an older car

Loan amounts

Loan amounts are usually lower on used car loans than they are on new car loans.

This one is simple. New cars cost more than used cars. Naturally, new car loans are bigger. As a rule, the more you borrow, the more interest you’ll pay (unless you have a great rate and you pay your loan off early).

- New car loans: Generally have higher loan amounts

- Used car loans: Generally have lower loan amounts

Incentives

Incentives are almost always better on a new car than they are on used cars.

Manufacturers often offer cash rebates and low or no interest for a certain amount of time (called an introductory period). The only manufacturer incentives you’ll typically find on a used car are on certified preowned vehicles.

- New car loans: Generally have more incentives

- Used car loans: Fewer incentives, if any

Loan terms

Loan terms are usually longer on new car loans than on used car loans.

The bigger the loan, the more time you’ll probably need to pay it off. In some instances, you can finance a new car for up to 84 months (seven years).

A long car loan might seem nice. You’ll probably have a lower monthly car payment. In reality, you should choose the shortest loan term you can comfortably manage. This’ll help you save total interest and make it less likely you end up owing more than the car is worth.

- New car loans: Generally have longer loan terms

- Used car loans: Generally have shorter loan terms

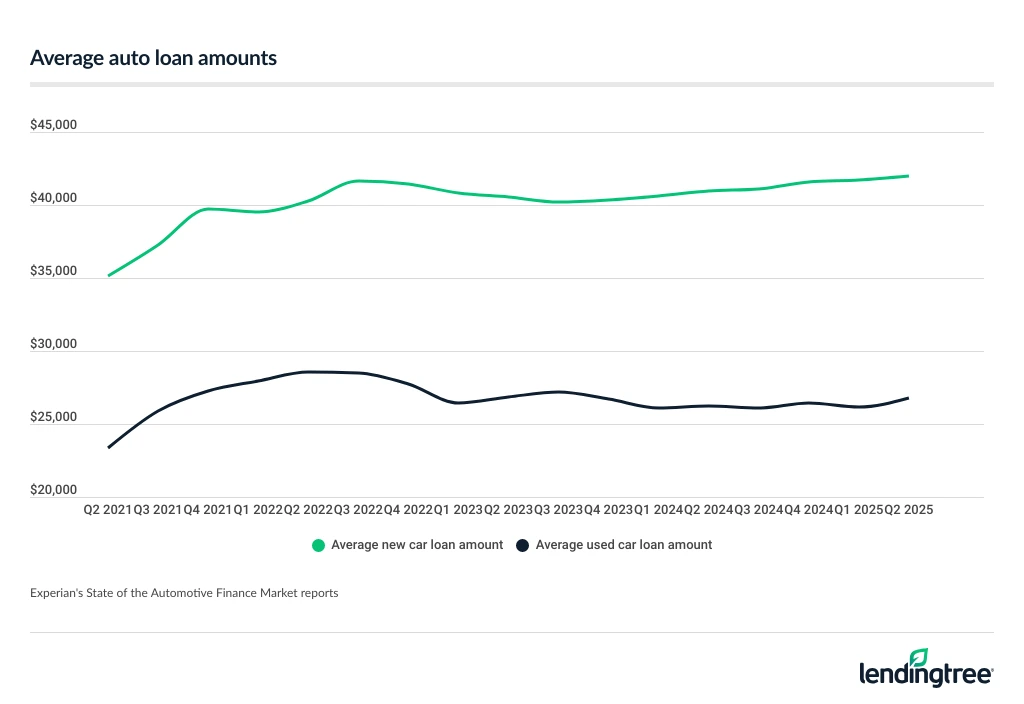

Car prices are rising, and the loan amounts show it

Car prices have taken drivers on a ride — and loan amounts have followed. From pandemic-driven supply shortages to inflation and new tariffs, financing trends can offer surprising insight into where the auto market is headed.

Use the graph below to see how loan amounts have increased over time. Although you can’t predict exactly where car prices are headed, trends can help you compare your car price to the highs and lows.

In Q2 2021, new car loans averaged slightly above $35,000, but peaked to nearly $42,000 in Q2 2025 and remain elevated. Used car loans, which surged during the used car boom, have started to moderate — offering potential value for buyers.

What this means for you

- Looking to buy soon? Comparing today’s trends to historical peaks can help you negotiate better — or wait if prices seem inflated.

- Refinancing? Understanding average loan sizes gives you leverage in rate shopping and loan terms.

- Used versus new? As used car loans cool off, the total cost of ownership may now favor used vehicles again — but only in the right conditions.

A LendingTree survey found that more than 3 in 4 (77%) Americans worry that tariffs will drive up the cost of owning a car. In fact, the majority of those who bought a car in 2025 did so earlier than they planned in order to get ahead of tariffs (81%).

Avoid car-buying mistakes with our expert insights

As a former dealer, what was the biggest mistake you saw car buyers make?

The most common mistake when buying a car is saying yes to a monthly payment. When you’re talking about money, do one thing at a time.

Get an agreement on the price of the car you want, then the price for your trade-in — if you have one — and, finally, the rate of your car loan.

If you agree to a monthly price first, the dealer will do everything to keep near that payment while increasing their bottom line. They could up your APR, up the length of your loan or try to slip in things like an extended warranty.

What sets LendingTree content apart

Expert

Our personal loan writers and editors have 32 years of combined editorial experience and 28 years of combined personal finance experience.

Verified

100% of our content is reviewed by certified personal finance professionals and meets compliance and legal standards.

Trustworthy

We put your interests first. We’ll tell you about any loan drawbacks and be clear about when to consider alternatives.

Frequently asked questions

In Q2 2025, LendingTree marketplace data showed average car loan rates ranging from around 7.00% for excellent credit on new cars to over 22.00% for credit scores under 580 on used cars.

Based on our unbiased, expert analysis, the best places to finance a car are:

- : Best for short-term loans with cheap rates

- : Best for car shopping and comparing sticker prices

- : Best for those with military ties

- Southeast Financial Credit Union (SFCU) : Best for bad credit auto loans

- Bank of America : Best for private-party auto loans

- Southeast Financial: Best for used car loans

- Autopay : Best car loan overall

- Navy Federal Credit Union (NFCU) : Best for those who prefer big banks

- Navy Federal Credit Union (NFCU) : Best for an online experience

- Digital Federal Credit Union (DCU) : Best for quick car loans

- Capital One : Best for dealerships in the Chase network

Boosting your credit score, putting down a big down payment, shopping around and comparing offers, getting a cosigner — these are all things that could help you get a lower auto loan rate. Use LendingTree and compare offers from up to five lenders for free, with no impact to your credit.

Usually, yes. Per law, federal credit unions can’t charge auto loan interest rates above 18.00%. However, you usually have to meet some sort of membership requirement. LendingTree’s network includes credit unions, banks and online lenders so you can compare all in one place.

Yes, it’s possible, but you will likely pay a high rate. If you don’t have time to improve your credit before buying a car, your best bet would be to shop with bad credit car loan lenders.

You can also boost your odds by:

- Adding a cosigner

- Putting down a larger down payment

- Picking a shorter loan term

- Choosing a cheaper car

No, checking rates with LendingTree won’t hurt your score. We use a soft credit inquiry when we shop for you. If you move forward with the loan, the lender will then run a hard credit check. This can drop your score by a handful of points.

Auto loan rates are usually negotiable, but it depends on where you’re buying your car. Some dealerships, including Navy Federal Credit Union (NFCU) , don’t negotiate — however, most dealerships are willing to haggle. You might have luck by bringing in a preapproved car loan and asking the dealer to beat its rate.

Our methodology

Accessibility. We look for lenders with fewer barriers to approval and award points for lower credit requirements, nationwide access, fast funding and simple applications.

Rates and terms. We prioritize lenders that offer low starting rates, minimal fees, flexible terms and APR discount opportunities.

Repayment experience. We choose lenders with strong reputations, convenient self-service tools, responsive support and borrower-friendly perks.

We reviewed 25 auto loan lenders to determine the overall best 11 lenders by these metrics. According to our systematic rating and review process, the best auto loans come from Southeast Financial Credit Union, PenFed Credit Union, Navy Federal Credit Union (NFCU), Autopay, PNC Bank, Digital Federal Credit Union (DCU), Capital One, Bank of America, CarMax, LightStream and Chase Bank. LendingTree reviews and fact-checks our top lender picks on a monthly basis.

Why trust our methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor℠, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.